Insurance Bonds (also known as Investment Bonds) are tax effective investment products offered by some life insurance companies.

There are three main points you need to understand when it comes to these investment products.

Tax rate of 30%

Instead of distributions or interest income being taxed in your hands like shares or savings accounts, the bonds themselves are taxed, less imputation credits, at a flat 30% per annum.

Ten Year Rule

If you maintain the Insurance Bond for 10 years then the original amount plus accumulated net of tax earnings can be withdrawn free of Capital Gains Tax (CGT) or any other personal income tax. As the tax benefits on withdrawals kick in after 10 years has elapsed they should be considered long term investments.

125% Rule

A major benefit of these products is the 125% Rule. Essentially it means that you can contribute up to 125% of the previous years investment amount and the new amount invested will assume the investment date of the original investment.

This is beneficial because it means that you can continue to make investments into the the bond over subsequent years and withdraw the funds on the tenth anniversary under the 10 year rule and not pay CGT.

For example, if in the first year you invest $1,000 then in the second year you can invest up to $1,250 and it will have the same start date as the original amount invested. In the third year you can invest up to 125% of the $1,250 and so it goes on for as long as you maintain it. You do not have to withdraw your funds in the tenth year and can maintain it as long as it is supported by the product provider.

[ad#Google Adsense – 468×60]

Extremely Important: If you miss a year of regular investments and then restart them in a subsequent year, the 10 year period starts again for the entire amount invested. Also, if you exceed the 125% amount the 10 years period starts again. It is therefore probably very important not to stop and then start annual investments or increase annual contributions greater than 125% amount of previous years.

What are Insurance Bonds Good For?

Long Term Savings for High Tax Payers

If your marginal rate of tax is higher than the 30% which is levied on Insurance Bonds then you potentially save tax on earnings.

Long Terms Savings for Children

Parents can invest on behalf of children and nominate a future age where the ownership transfers to the child. Children or minors are subject to special rates of tax which might make holding large investments in their own name not as tax effective.

Investment Options

These products can invest into basically any asset class with many providers offering a wide range of investment choices.

Any imputation credits received from shares can be used to offset income tax payable.

Changing investment options unlike managed funds or superannuation for that matter does not trigger CGT.

Nominate a Beneficiary

You can nominate a beneficiary to receive the proceeds if you pass away. This will ensure that funds go directly to those nominated and will not be dealt with by your estate.

Access or Early Withdrawal

You can withdraw all or part your investment at any time subject to the minimum balance conditions imposed by the product provider but there are tax consequences you should understand.

Withdrawals before 8 years has passed: investment growth is included in your assessable income although you will receive a tax offset for the 30% tax that was deducted in previous years.

Withdrawals in the 9th year: one third of the growth is treated as tax paid with the remainder treated as assessable income and you again receive the tax offset for previous tax levied.

Withdrawals before the end of the 10th year: two thirds of the investment growth is treated as tax paid and the remaining third is treated as assessable income and you receive the tax offset for previously levied tax.

Summary Points

- Earnings taxed at a flat 30%. Tax paid by the bond.

- Ten year rule. Capital gains tax and personal income tax free after 10 years.

- 125% Rule – regular annual investment of 125% gains 10 year rule benefits.

- Danger – exceeding the 125% amount or stopping then starting annual investments restarts the 10 year tax free period.

- Potential tax advantages for long term savings – for children and high tax paying individuals.

Here’s a list of pros and cons of insurance bonds (also known as investment bonds) specifically within the Australian consumer context:

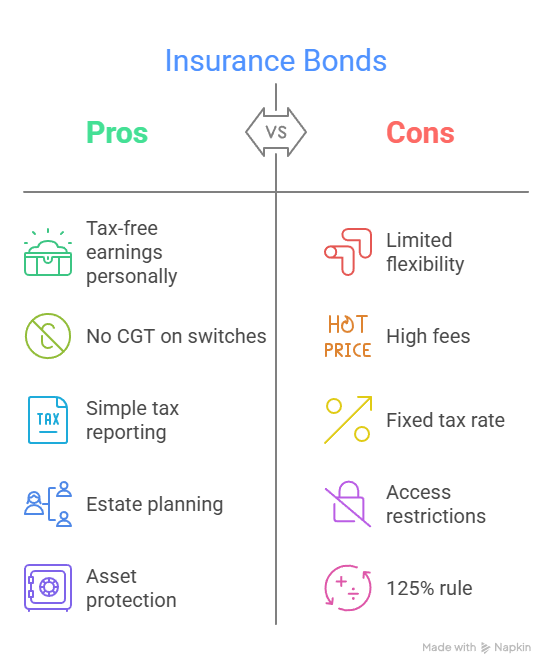

Pros of Insurance Bonds

1. Tax Effectiveness (Especially Long-Term)

- After 10 years, earnings within the bond are tax-free if no additional contributions break the 125% rule.

- Tax is paid at the company rate (30%), potentially lower than the marginal tax rate for high-income earners.

2. No Capital Gains Tax (CGT) for Switching Investments Within the Bond

- Internal asset switches within the bond structure do not trigger CGT, unlike managed funds.

3. Simplicity in Tax Reporting

- No need to declare annual earnings on your tax return if you follow the rules, unlike managed funds or shares.

4. Estate Planning Benefits

- Proceeds can be paid directly to nominated beneficiaries tax-free upon death of the policyholder.

- Can bypass probate and avoid family disputes.

5. Asset Protection

- May offer some protection from creditors or family law claims, depending on structure.

6. Child Advancement

- Can be used for education savings and automatically transferred to a child after a nominated age.

Cons of Insurance Bonds

1. Limited Investment Flexibility

- Fewer investment options than direct investing or managed funds.

- May be limited to in-house funds of the provider.

2. Fees Can Be High

- May include entry fees, ongoing management fees, and adviser commissions depending on the provider.

- Less transparency on fee structure than some modern platforms.

3. Tax Rate Is Fixed

- Earnings are taxed at 30%, which may be higher than the marginal tax rate for low-income earners or retirees.

4. Access Restrictions

- Not suitable for short-term savings; early withdrawals may incur tax penalties unless carefully managed.

5. 125% Rule Complexity

- To maintain tax-free status after 10 years, additional contributions must not exceed 125% of the previous year’s.

- Breaking this resets the 10-year rule.

6. Market Risk

- Like all investment products, subject to market fluctuations and potential loss of capital.

Disclaimer: Investment product features, details, related tax rules and other legislation change without notice. It is highly recommended that you seek advice from a Financial Planner before taking any action.

Insurance Bond Providers

Comminsure Investment Growth Bond

ING Investment Savings Bond